MEMO

TO: Hon. John Hanlin

Douglas County Sheriff

FROM: People of Douglas County ex rel.

Paul Andrew Mitchell, B.A., M.S.

Private Attorney General (18 U.S.C. 1964)

DATE: September 1, 2019 A.D.

SUBJECT: major accounting discrepancies in

Douglas County’s published financial statements

Greetings Sheriff Hanlin:

The People of Douglas County respectfully request a full investigation of major accounting discrepancies which this MEMO seeks to document and summarize with our studied observations and recommendations.

In the process of subjecting the attached Exhibits to very close scrutiny, we wish to warn you, in advance, that such an effort may be boring, confusing, or both. In order to simplify this MEMO as much as possible, permit us to begin with a relevant example.

Let’s say that your friends invite you to a New Year’s Eve party, but you decide to stay home and go to bed early, before midnight. Your bank debit card balance is $100, and you do not loan your debit card to any of the party goers. As such, your balance at 1 second before midnight should be exactly the same as your balance at 1 second after midnight. The only thing that has changed is the transition to a new calendar year at midnight starting a New Year.

In the analysis that follows, please keep this simple example foremost in your mind. For purposes of this MEMO, the only difference is that the transition that matters is the change in Douglas County’s Fiscal Year (“FY”) that occurs as the calendar moves from June 30 to July 1 in any given calendar year. With that difference in mind, let’s dive into the details now.

The attached Exhibit “C” demonstrates how Douglas County’s required Comprehensive Annual Financial Reports (“CAFR”) do exhibit an exact equivalence between the “Fund balances, ending” on June 30 and the “Fund balances, beginning” on July 1, as follows:

FY 2014-2015 FY 2015-2016 FY 2016-2017 FY 2017-2018

------------ ------------ ------------ ------------

Beginning Balances:

$162,507,948 $150,400,300 $146,389,082 $132,960,175

Ending Balances: $150,400,300 $146,389,082 $132,960,175 $126,501,269

The ending balance on June 30, 2015 was $150,400,300 and the beginning fund balance on July 1, 2015 was also $150,400,300.

The ending balance on June 30, 2016 was $146,389,082 and the beginning fund balance on July 1, 2016 was also $146,389,082.

The ending balance on June 30, 2017 was $132,960,175 and the beginning fund balance on July 1, 2017 was also $132,960,175.

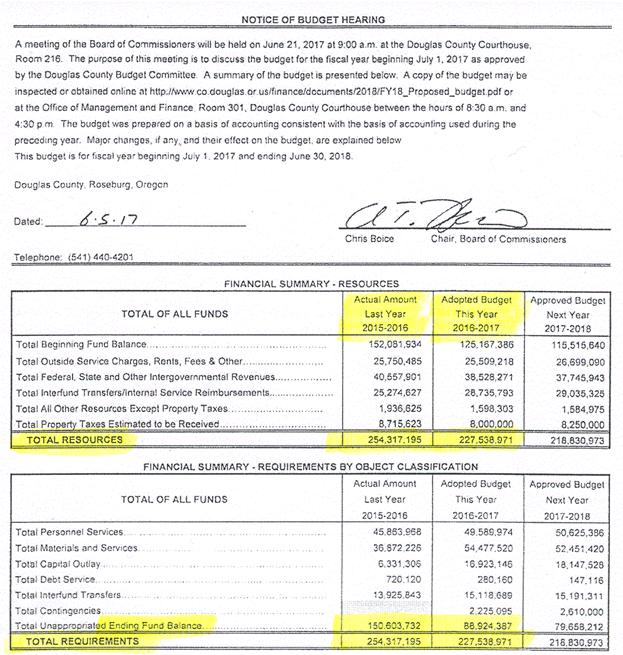

The comparable summaries in attached Exhibit “A” do NOT reflect the same equivalence, however. Please focus on the following numbers in Exhibit “A”:

Actual Amount Adopted Budget

Last Year This Year

2015-2016 2016-2017

------------- --------------

Beginning Fund Balance: $152,081,923 $125,167,386

TOTAL RESOURCES: $254,317,195 $227,538,971

Ending Fund Balance: $150,603,732 $88,924,387

TOTAL REQUIREMENTS: $254,317,195 $227,538,971

We have highlighted two numbers in bold type, to help you focus on the sheer size of the arithmetic difference between them:

$150,603,732 - $125,167,386 = $25,436,346 USD

===============

We have honestly tried to reconcile the latter discrepancy with the audited CAFRs, but that honest attempt was not successful.

In particular, the NOTICE OF BUDGET HEARING in Exhibit “A” was signed by Commissioner Chris Boice on 6-5-2017. The CAFR for any given Fiscal Year requires about six (6) months for the independent auditors to complete and publish. This means that the “Actual Amounts” for the FY ending June 30, 2016, were already available to Commissioner Boice for approximately six full months by June 5, 2017.

The CAFR for FY ending June 30, 2016 shows the following numbers for “Fund balances, beginning” and “Fund balances, ending”:

Actual Amount

Fiscal Year

2015-2016

-------------

Beginning Fund Balances: $150,400,300 (compare above)

Ending Fund Balances: $146,389,082 (compare above)

The CAFR for FY ending June 30, 2017 shows the following numbers for “Fund balances, beginning” and “Fund balances, ending”:

Actual Amount

Fiscal Year

2016-2017

-------------

Beginning Fund Balances: $146,389,082

Ending Fund Balances: $132,960,175

To repeat, the ending balance on June 30, 2016 was $146,389,082 and the beginning fund balance on July 1, 2016 was also $146,389,082 i.e. exactly equivalent.

Another confusing discrepancy is discovered by comparing Adopted Budget and Revised Budget figures from the Combined Summaries of Budgeted Resources and Requirements. (See Exhibit “D” attached).

By extracting Beginning Balances, Revenues, Expenditures and Ending Balances, we summarize the Adopted and Revised Budgets for Fiscal Year 2016-2017, using actual data from Exhibit “D”, as follows:

Adopted Budget Revised Budget

Fiscal Year Fiscal Year

2016-2017 2016-2017

-------------- --------------

BEGINNING FUND BALANCES: $125,139,536 $125,167,386

Total Revenues: +$100,378,064 +$102,376,585

Total Expenditures: -$136,593,213 -$138,619,584

ENDING FUND BALANCES: $88,924,387 $88,924,387

We have highlighted with bold type the BEGINNING and ENDING FUND BALANCES showing in the Revised Budget for Fiscal Year 2016-2017. ENDING FUND BALANCES are identical in both columns immediately above.

The attached Exhibits justify the inference that a Proposed Budget becomes an Adopted Budget when approved by the Commissioners. Then, during a Fiscal Year, an Adopted Budget is routinely amended to produce a Revised Budget for that same Fiscal Year. Finally, at the end of a Fiscal Year, the Revised Budget is followed by an independent audit which shows Actual Amounts for all key totals.

This additional analysis shows that the second column heading in the NOTICE OF BUDGET HEARING, signed by Chris Boice on June 5, 2017, is incorrect. It reads “Adopted Budget” [sic], “This Year”, “2016-2017”.

However, in that NOTICE OF BUDGET HEARING, the totals for “Beginning Fund Balance” and “Ending Fund Balance” were exactly equal to the corresponding figures in the Revised Budget for Fiscal Year 2016-2017 (see above).

The audited CAFR for any given Fiscal Year is typically published in December, some six (6) months after the end of the FY being audited.

In the CAFR for FY 2016-2017, the beginning fund balance on July 1, 2016 was reported as $146,389,082; the ending fund balance on June 30, 2017 was reported as $132,960,175. (See Exhibit “C” attached.)

By comparison, the Revised Budget for Fiscal Year 2016-2017 shows a beginning fund balance of $125,167,386 and an ending fund balance of $88,924,387. (See Exhibit “D” attached.)

Once again, although not as large as the $25.4 Million discussed above, the calculated difference between the CAFR’s beginning fund balance, and the corresponding figure in the Revised Budget for Fiscal Year 2016-2017, is still very large:

$146,389,082 - $125,167,386 = $21,221,696

===========

The calculated difference between the CAFR’s ending fund balance, and the corresponding figure in the Revised Budget for FY 2016-2017, is also very large:

$132,960,175 - $88,924,387 = $44,035,788

===========

The People of Douglas County hereby encourage your office to study the attached Exhibits in detail sufficient to arrive at your own professional, and defensible, conclusions.

We believe the following questions warrant honest and verifiable answers that also deserve timely publication and open public discussion, to wit:

Question #1: Why is there an obvious discrepancy of $25.4 Million on the NOTICE OF BUDGET HEARING signed by Chris Boice on June 5, 2017? (See Exhibit “A” attached.)

Question #2: Why is the “Actual Amount” of the “Ending Fund Balance” for FY 2015-2016 not exactly the same as the “Beginning Fund Balance” on the “Adopted Budget” for FY 2016-2017? (See Exhibit “A” attached.)

Question #3: Why does that NOTICE OF BUDGET HEARING not show the comparable amounts that do show in Douglas County’s CAFR, as prepared and published by an independent auditor? (We understand that the CAFR for FY ending June 30, 2019, will not likely be available before December 2019.) Why are CAFR figures not used when available?

Question #4: Exhibit “B” also shows a budget process that publishes a notice of budget hearing and budget summary in mid-June of each FY. We have now requested three (3) subsequent NOTICEs OF BUDGET HEARING showing “Actual Amounts” for FYs 2016-2017, 2017-2018 and 2018-2019, respectively. Why have we not received any acknowledgment or reply(s) to that Public Records Request? Actual amounts for FY 2018-2019 should be available by now (September 2019), even if the CAFR is not.

Question #5: In particular, our Public Records Request also requested directions for locating those same NOTICEs OF BUDGET HEARING at Douglas County’s Internet website. Why are those same NOTICEs not already published and available to the public at Douglas County’s Internet website? (See Exhibit “B” attached.)

Question #6: Are Douglas County’s financial officers maintaining two (or more) different sets of books; and, if so, for how long has this been the practice of Douglas County’s financial officers? This same question has already arisen, and remains outstanding (not answered), in connection with the DOUGLAS COUNTY DAMAGES CLAIM dated 5/24/2017.

Question #7: Why are there such large discrepancies when comparing audited CAFR summaries with the corresponding figures in Douglas County’s Proposed, Adopted and Revised Budgets?

We look forward to receiving written notice from your qualified Deputies, delegated by your good Office with the task of finding and publishing verifiable answers to all of the questions itemized above.

The unjustified “disappearances” of $25.4 and $44 Million are frankly much too large to be stubbornly ignored by all responsible personnel.

Thank you very much, Sheriff Hanlin, for your committed professional consideration in this important fiscal matter.

Sincerely yours,

/s/ Paul Andrew Mitchell

Paul Andrew Mitchell, B.A., M.S.

Private Attorney General, Civil RICO: 18 U.S.C.

1964;

Agent of the United States as Qui Tam Relator (4X),

Federal Civil False Claims Act: 31 U.S.C. 3729 et

seq.

All Rights Reserved

(cf.

UCC 1-308 https://www.law.cornell.edu/ucc/1/1-308)

Attachments:

http://supremelaw.org/cc/DoCo/sheriff/letter.2019-08-07/email.2019-08-07.htm

http://supremelaw.org/cc/DoCo/sheriff/letter.2019-08-08.1/email.2019-08-08.1.htm

http://supremelaw.org/cc/DoCo/sheriff/letter.2019-08-08.2/email.2019-08-08.2.htm

http://supremelaw.org/cc/DoCo/sheriff/letter.2019-08-10/email.2019-08-10.htm

Exhibit “A:” NOTICE OF BUDGET HEARING, June 5, 2017

Exhibit “B”: Budget

Calendars of the Event:

"Publish notice of budget hearing"

http://www.co.douglas.or.us/finance/documents/2020/FY19-20GeneralInfo.pdf

http://supremelaw.org/cc/DoCo/2020budget/FY19-20GeneralInfo.pdf

Publish notice of budget hearing and budget

summary June 12, 2019

http://www.co.douglas.or.us/finance/documents/2019/FY18-19GeneralInfo.pdf

http://supremelaw.org/cc/DoCo/2019budget/FY18-19GeneralInfo.pdf

Publish notice

of budget hearing and budget summary June 13, 2018

http://www.co.douglas.or.us/finance/documents/2018/FY17-18GeneralInfo.pdf

http://supremelaw.org/cc/DoCo/2018budget/FY17-18GeneralInfo.pdf

Publish notice

of budget hearing and budget summary June 14, 2017

http://www.co.douglas.or.us/finance/documents/2017/FY16-17GeneralInfo.pdf

http://supremelaw.org/cc/DoCo/2017budget/FY16-17GeneralInfo.pdf

Publish notice

of budget hearing and budget summary June 15, 2016

http://www.co.douglas.or.us/finance/documents/2016/FY15-16GeneralInfo.pdf

http://supremelaw.org/cc/DoCo/2016budget/FY15-16GeneralInfo.pdf

Publish notice

of budget hearing and budget summary June 3, 2015

Exhibit “C”: Comprehensive Annual Financial Reports

http://co.douglas.or.us/

http://supremelaw.org/cc/DoCo/2018cafr/CAFR.2018.pdf

(Adobe page 5

of 40)

http://co.douglas.or.us/

http://supremelaw.org/cc/DoCo/2017cafr/CAFR.2017.pdf

(Adobe page 5

of 40)

http://co.douglas.or.us/

http://supremelaw.org/cc/DoCo/2016cafr/CAFR.2016.pdf

(Adobe page 6

of 41)

http://co.douglas.or.us/

http://supremelaw.org/cc/DoCo/2015cafr/CAFR.2015.pdf

(Adobe page 6

of 43)

Exhibit

“D”: Combined Summaries of Budgeted Resources and Requirements

http://co.douglas.or.us/

http://supremelaw.org/cc/DoCo/

http://co.douglas.or.us/

http://supremelaw.org/cc/DoCo/

http://co.douglas.or.us/

http://supremelaw.org/cc/DoCo/

http://co.douglas.or.us/

http://supremelaw.org/cc/DoCo/

http://co.douglas.or.us/

http://supremelaw.org/cc/DoCo/